National Pension System(NPS) in India is a Govt. regulated Pension Investment Product. It is also considered to be Ultimate Retirement Solution as it is highly cost effective, Tax efficient Product enforces discipled investment towards Retirement Savings. There are two Types of NPS (Tier I and Tier II) with multiple types of Fund options provided by various different Pension Fund Companies.

NPS is regulated to PFRDA (India Govt Authority). To invest in NPS, every investor has to create a unique account number called PRAN (a Pension ID, Similar to PAN number as Tax ID).

NPS investment can be done Privately by individuals or by employer (as Salary deduction/contribution). However, in this page, we only look at NPS investment by Individuals. Just like Mutual Funds and other investments in India, along with resident Individuals, NRIs and OCIs are allowed to invest in NPS.

NPS types , their benefits and taxation

There are two types of NPS

Tier I : This is the primary Pension product. Investment can be done till 60 years of age. After 60 years till 75 Years of Age 60% of total investment corpus can be withdrawn Tax Free (through multiple partial withdrawal or one time full withdrawal). Remaining 40% of the investment corpus has to be received as monthly pension. No Withdrawal possible before 60 years, which allows the invest corpus to grow and not get disturbed by any short term monetary needs. Up to 75% of the investments could be contributes to Equity and 25% must be invested in some other fund (Govt Security or Corporate Debt Funds or Alternate Investment Fund). NPS provides option of switching between Fund Managers and Types of funds.

Tier I investment provides 1.5 Lakhs of Tax savings through 80 C (along with many other Tax savings options) and on top it provides additional 50 Thousand Rupees Tax savings through 80CCD exclusively applicable for NPS. Even NRI/OCIs having some kind of income in India can use this tax savings.

Tier II : This is very similar to Mutual Fund Savings scheme. Investment can be done in any scheme and even 100% in Equity possible. Fund switching is allowed here as well. Any amount of Fund can be withdrawn at any time. There is also option of one way switch of Tier II fund to Tier I fund. This is an useful option as investors who are not looking for any tax savings option can contribute to this fund. It remains liquid (any emergency withdrawal possible with one click). During the retirement phase, Tier II investment can be transferred to Tier I investment and all tax benefit of Tier I maturity can be availed.

For Taxation purpose, the Gains/returns of the funds are treated as regular income during withdrawal. Unlike Mutual Fund gains, there are no Long Term or Short Term capital gains treatment for Tier II NPS.

Low Cost Structure and Comparison with other Pension Alternatives

The Fund Management charges are extremely low in NPS , typically less than 0.1% even for Equity Funds. This is extremely low compared to the Fund Management charges for other Equity investment Alternatives in India and even globally. It is just 5-10% of what Mutual Fund Pension Funds or Insurance Company Pension funds charges. This is the most attractive part of NPS. For a long term Pension product, in which investor contributes for multiple decades, the big difference of Fund Management charges can significantly enhance the retirement corpus for NPS, in comparison with other products.

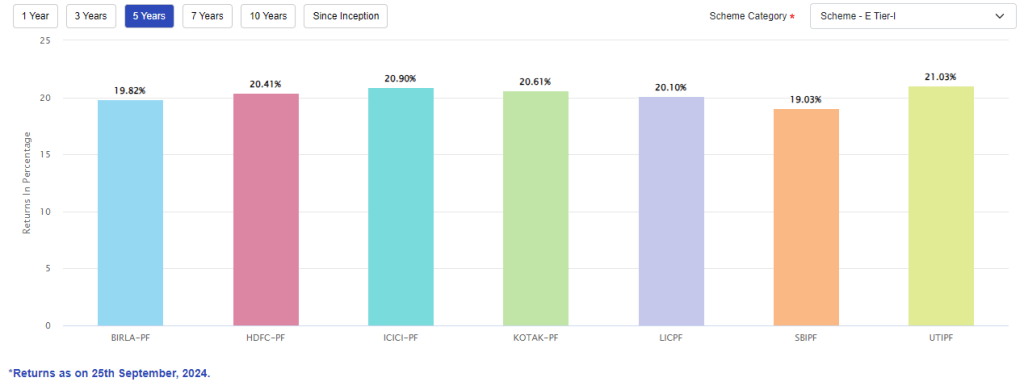

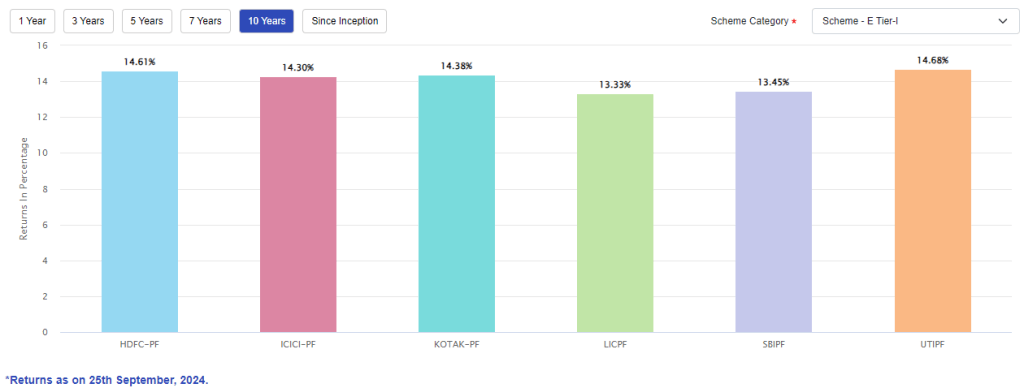

NPS investment returns at a glance

As seen above 5 and 10 years returns of the Equity Funds are at par with the Diversified Equity Mutual Funds.

Invest in NPS

Through us, you could invest in all types of NPS schemes from almost all Pension Fund Houses. We could guide you through the account creation process as well setting up long term periodic investment mechanism as well as guide through time to time Fund Switch recommendations based on various factors.